Make / Model Search

News - Market Insight - Market Insight 2020Market insight: Vans reflect Australian economyBad sign: Van sales are usually a good indicator of economic health, which makes for troubling reading in Australia. Small business stalls as van sales slide and economic health weakens Gallery Click to see larger images 5 Oct 2020 By NEIL DOWLING LOOK around your city – if little vans don’t appear to be as common as they were a year ago, there is a frightening reason.

Van sales have often been linked directly to the economic status of a city and in turn, the health of the country. The rationale is that small business runs on delivery vans and the more vans in use, the more work being generated by small businesses.

If that was the case, then Australia is showing signs of a weakened economy and few would argue that a pandemic hasn’t helped the majority of small businesses.

Roll back a decade and when the world was crawling out of the Global Financial Crisis, the Australian van market in the nine months to September 2010 was slightly down 0.2 per cent and sales in the period stood at 17,782. In 2020, there’s 14,268 sales.

Five years later, the Australian economy was just about to be hit by the end of the mining boom but the nine months of 2015 showed total vehicle sales up 3.6 per cent while vans under 2.5-tonnes had a 24.2 per cent growth and the vans in the 2.5-tonne to 3.5-tonne segment were up 9.7 per cent.

But the GFC and the mining slump have nothing on 2020. To counter the balance and keep buyers interested, the federal government enlisted a lot of incentives including the instant asset writeoff for taxation which gave a boost to the entire LCV market. It was, however, a bit of a flash in the pan and failed to sustain the van sales.

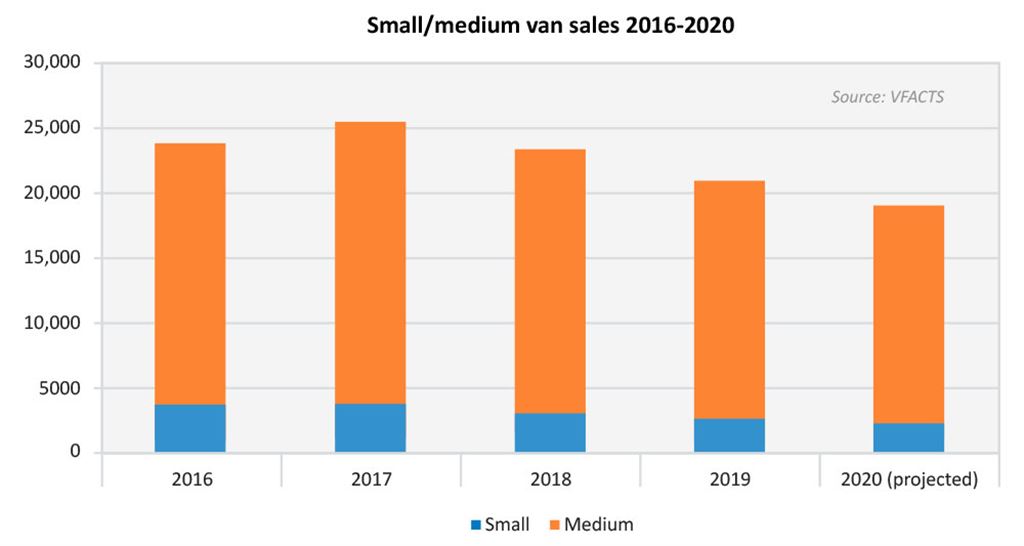

In 2020, just over 14,000 vans in the two sub-3.5-tonne categories – which are the ones used more for CBD and suburban deliveries – were sold in the year ending September 30, down almost 10 per cent on the same period in 2019.

With the slide in sales, there also came a withdrawal from the market of the Citroen LCV models – the Berlingo and Dispatch – with the Peugeot clones taking over the nameplate’s van territory.

Now there are 14 vans on the landscape, boosted recently with the launch of the Mitsubishi Express, becoming an old name for a new model which is itself actually not a Mitsubishi.

Confused? The Express is a rebadged and reconfigured Renault Trafic. The same cloning exercise was applied to the Citroen Berlingo (Peugeot Partner) and Citroen Dispatch (Peugeot Expert) before the Citroens were withdrawn and Peugeot became the parent company’s Australian LCV brand.

There were even dalliances between Ford, Peugeot, Renault, Vauxhall and Toyota but, thankfully, normality is returning to the market.

Vindicating the theory that city finances are mirrored in light-van activity is the sub-2.5-tonne van market which this year is down 14.3 per cent on the same period in 2019.

There are four players after Citroen’s exit last year – Fiat Doblo, Peugeot Partner, Renault Kangoo and Volkswagen Caddy, with the sole German contender taking the lion’s share thanks to a 68.4 per cent slice of the segment.

The Caddy has no upcoming threat and is almost assured of the segment crown given it will launch in its fifth generation in Australia early next year with a platform based on the Mk8 Golf small car.

Volkswagen has sold 1201 Caddys this year, down 10.5 per cent but above the segment’s average fall of 14.3 per cent. It was the least affected by the economic downturn, with rivals down up to 42 per cent on their 2019 figure.

The bigger van segment for the 2.5-tonne to 3.5-tonne vehicles was also down in year-to-date figures, with an average fall between brands of 9.1 per cent.

The suffering wasn’t as bad as the smaller van brands, with the only real standout loser being the Volkswagen Transporter as Covid-19 affected production and supply just as the factory turned over to the T6.1 upgrade, expected here next month.

Volkswagen sold 472 Transporters this year for a 3.8 per cent share. The Transporter is currently only available as California Beach and Multivan Cruiser limited edition variants until the T6.1 series gets here, oddly soon to be followed in 2021 by the T7 series that has already been seen in Europe.

The medium-size van segment was dominated – again – by Toyota with the Hiace selling 4460 units to the end of September for a 35.6 per cent share. Toyota sales of the Hiace – overhauled in 2019 – were down 1.2 per cent on the same period last year.

Strong results were shown by Mercedes-Benz Vito sales with 889 new owners and a 7.1 per cent market share, a jump of 201.4 per cent on the corresponding period in 2019.

The rise was attributed to an increased range of variants under the Vito label and some movement during the period from a low base. Mercedes-Benz will overhaul the Vito early next year with a new nose and more features for the expectation of more sales.

Peugeot’s Expert also leapt in sales, up 151.5 per cent year-to-date, again from a low base. It has sold 166 units this year.

The only other increase was from the well-received Ford Transit Custom which posted 1568 sales for a 12.5 per cent share, up 2.6 per cent on 2019.

The rest stumbled. Hyundai’s iLoad was down 27.9 per cent on 2019 despite strong sales of 2300 units and a second-place 18.4 per cent market share.

The Renault Trafic was down 19.4 per cent (1120 sales to date for 9.0 per cent market share) and the two Chinese LDVs were down 11.9 per cent and 13.8 per cent for the G10 and V80 vans respectively.

Sales of these two are still healthy, with the G10 finding 920 owners and the V80 with 349 and segment market shares of, respectively, 7.4 per cent and 2.8 per cent.

Despite the slide in sales, vans remain a powerful tool in a car-maker’s arsenal.  Read more28th of September 2020  Market Insight: BMW M chasing record sales in 2020Australian BMW M sales are up 6.1 per cent so far this year ending August21st of September 2020  Market Insight: SUVs take toll on hatchbacksLight car segment sinks on COVID, rising prices, shrinking choice and SUV appeal |

Click to shareMarket Insight articlesResearch Market Insight Motor industry news GoAutoNews is Australia’s number one automotive industry journal covering the latest news, future and new model releases, market trends, industry personnel movements, and international events. Car Finance |

Connect with us

Facebook Twitter Instagram