Make / Model Search

News - Market Insight - Market Insight 2023Market Insight: Winners and losersShowroom showdown: Kia sales soared in 2022, helped by popularity and supply of the Sportage (left) while Nissan struggled with a depleted model range and big declines in Navara sales. We wade through 2022 VFACTS data to find the auto market’s biggest winners and losers Gallery      Click to see larger images 16 Jan 2023 By MATT BROGAN LAST week we looked at the sales charts for 2022, celebrating those manufacturers which had achieved strong numbers in another challenging year, and marvelling at an outright tally that nearly hit the 1.1 million vehicle mark (1,081,429 units).

But there is more to the story; vehicle buying trends among Australians are changing rapidly, not only with an increase toward electrification and new energy vehicles, but also in the types of vehicles we are purchasing – and from where they are sourced.

Interestingly, the data also shows that as the value offering of once run-of-the-mill brands push further upstream – creating space for newcomers beneath them – we see more and more buyers moving away from the top end of town and into higher-grade mainstream variants.

The tables and graphs GoAuto has prepared provide an overview of the Aussie market as a whole and offer an insight into where trends will swing in 2023 and beyond.

Spoiler alert: if you were selling well-equipped Chinese-made mid-size battery-electric SUVs right now you’d be sitting pretty.

Mainstream premium brands were down overall with Lexus crashing by 23.7 per cent (-2201 units), BMW 8.8 per cent in the red (-2195), Land Rover sliding 32.7 per cent (-2111), Mercedes-Benz cars slumping 5.5 per cent (-1547), Audi down 7.9 per cent (-1271) and Jaguar plummeting 42.7 per cent (-522) in sales against the full year of of 2021.

The only three to buck the trend were Volvo, which marched to an all-time record with 18.7 per cent growth (+1687 units), while Porsche soared 26.6 per cent (+1180) and Genesis climbed 41.6 per cent off a low base (up 305 units).

Biggest winner by volume shift: Volvo Biggest loser by volume shift: Lexus

Popular non-premium brands saw mixed results with Nissan showrooms bereft of stock and customers to the tune of 35.8 per cent (losing a massive 14,772 sales over 2021), Volkswagen 24.1 per cent behind its 2021 result (-9824 units), Ford down 6.7 per cent (-4752), Honda going backwards by 19.1 per cent (-3347), Mazda slipping 5.3 per cent (-5401) and Subaru reversing by 2.6 per cent (-979).

Kia had a ripper year, up 15.3 per cent (+10,366 units ), as did Mitsubishi with a 13.7 uplift (+9259), while Suzuki had a bonanza with a 23.5 per cent uptick (+4110), Toyota remained stable with 3.3 per cent more sales than in 2021 (+7408) and Hyundai remained in the black to achieve modest 0.6 per cent growth (+473).

Biggest winner by volume shift: Kia Biggest loser by volume shift: Nissan

Where fuel type is concerned, the move toward electrification is hard to ignore. Battery electric vehicle sales rose by almost the same number as petrol models fell (28,261 units versus -28,976 units), while diesel (+14,413) and hybrid (+11,320) models enjoyed similarly strong growth.

Biggest winner by volume shift: Electric Biggest loser by volume shift: Petrol

Country of origin statistics show that Australia’s love of Chinese-sourced cars is continuing to grow at a steady rate. The upswing toward vehicles produced in China was the strongest overall (+46,583 units), with Thailand (+15,088) and South Korea (+14,219) also tracking well.

However, vehicles produced in Japan took a nosedive in 2022 (-20,873 units) and English-built cars also took a dive (-9630).

Biggest winner by volume shift: China Biggest loser by volume shift: Japan

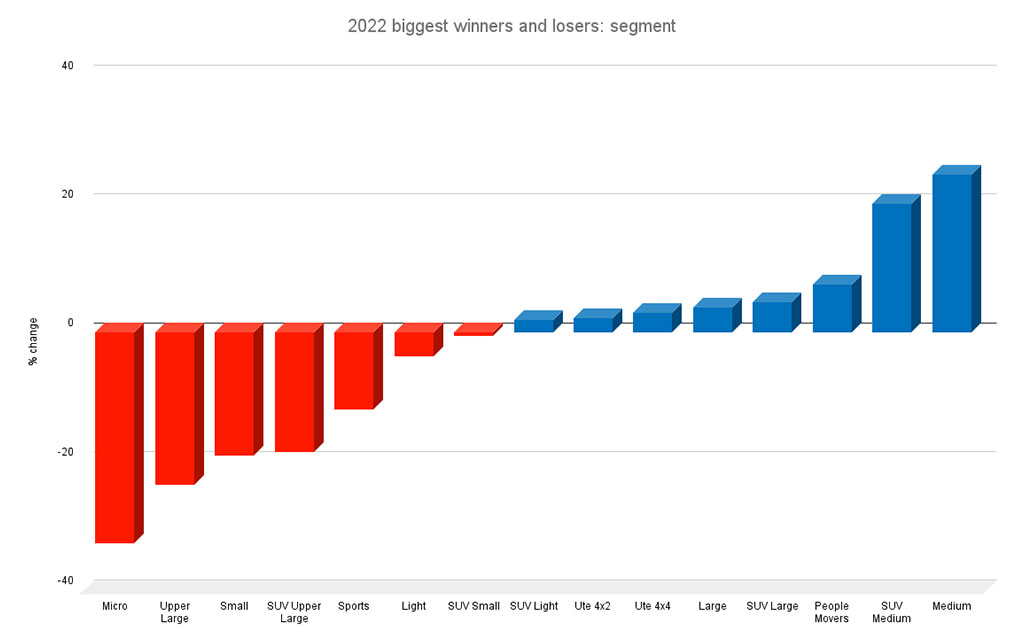

The sale of passenger vehicles in 2022 continued to decline against more popular SUV and light commercial models.

In percentage terms, micro cars fell the furthest with a 32.7 per cent drop over the year while light cars (-3.7 per cent) sales fell least.

Small cars (-19.1 per cent) took a hit, medium cars (+24.6 per cent) were up – buoyed by stronger sales of popular premium models – large cars (+3.9 per cent) went up slightly and the upper large segment (-23.7 per cent) was down considerably.

By comparison, SUV sales looked positively rosy. Excluding the small SUV segment (-0.5 per cent) and upper large SUV category (-18.5 per cent), every other SUV sector was ahead, with medium SUVs (+20.0 per cent) growing considerably over the previous year.

Despite being Australia’s best-selling car segment, the 4x2 and 4x4 ute categories grew only slightly in percentage terms during 2022, up 2.2 and 3.0 per cent respectively.

Biggest winner by percentage change: Medium cars Biggest loser by percentage change: Upper large cars

Model by model, it is evident that many of the big sellers in 2021 remained most popular in 2022. Segment by segment, we have highlighted the best and worst performers, showing where Australian favours lie when it comes to shopping by model.

In the micro car segment, the Kia Picanto topped the chart with 5196 sales ( -21.2 per cent), the light car segment saw buyers favour the MG 3 (13,774 units and +17.4 per cent), the premium light car segment was led by the Mini Hatch (1651 and -11.5 per cent), while the trusty Toyota Corolla (25,284 and -12.1 per cent) continued to dominate the mainstream small car segment.

Sitting atop the premium small car segment was the Mercedes-Benz A-Class with 2840 units sold, but this was down 25.1 per cent on the previous year’s sales.

Toyota’s Camry ruled the medium car segment once more in 2022 with an impressive 9538 sales. Though these were down significantly on the year prior (-27.1 per cent), the Camry did pip the second-placed Mazda 6 by an astonishing 8027 units.

On the premium side of the medium car segment the Tesla Model 3 led with 10,877 sales (no percentage available as this was Tesla’s first full year of VFACTS reporting), outselling the second-placed Mercedes-Benz C-Class by three to one.

For the dwindling large car segment the Kia Stinger (2242 sold, up 59.3 per cent led the mainstream market while the premium end was led by the BMW 5 Series (457 units, down 24.5 per cent). Upper large cars saw the now-defunct Chrysler 300 (79 sold, down 53.5 per cent) and BMW S-Class (167 units, down 36.5 per cent) top each side of the $100K divide.

The people mover segment was again dominated by the Kia Carnival in number-one spot (8054 deliveries, up 37.4 per cent), while among those prived above $60K, the Mercedes-Benz V-Class ruled the roost (570 sales, up 72.7 per cent).

Rounding out the passenger car classification with those classified as sports models, Ford’s Mustang was steady on top of the sub-$80K bracket (1887 sales, down 33.3 per cent), the BMW 4 Series topped the above-$80K category (1001 units, down 9.6 per cent), and the Porsche 911 took its usual spot on top of the above $200K category (547 delivered, up 27.8 per cent).

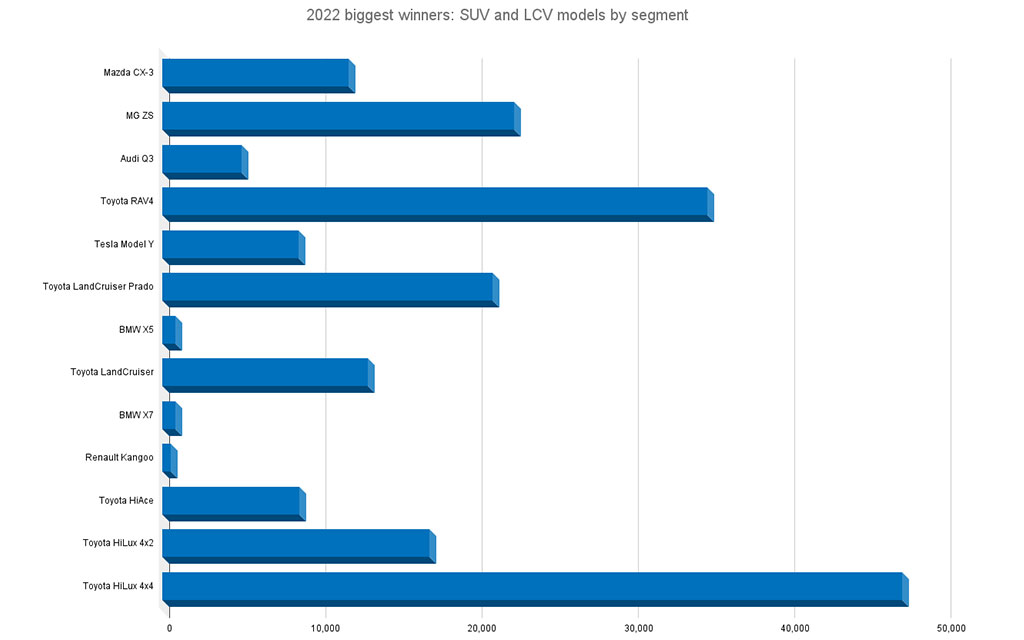

Walking through the SUV and LCV categories, it is easy to see how popular such models have become. Comparing the numbers of SUV and LCV variants sold against those in the passenger segment proves Australia is a nation in love with high-riding cars – particularly those with four-wheel drive ability and a tray up back.

At the light SUV end of the field, Mazda’s CX-3 remains a popular choice, selling 11,907 units over the course of 2022 (-7.5 per cent), while in the next segment up, the trajectory of the MG ZS seems almost unstoppable among small SUVs with 22,466 units sold (+21.9 per cent).

On the premium SUV side of the fence, the Audi Q3 remains a popular choice, with 5048 examples sold (-11.5 per cent).

The fiercely competitive medium SUV segment was topped by Toyota’s RAV4 (34,845 and -2.5 per cent) while Tesla’s Model Y sat atop the premium portion of the category with 8717 unit sales (no percentage available as this was Tesla’s first full year of VFACTS reporting), almost double that of the second-placed BMW X3 (4546 units, up 7.2 per cent).

Toyota also enjoyed wins in the large and upper large SUV segments where its LandCruiser Prado and LandCruiser chalked up 21,102 (-0.9 per cent) and 13,152 (-8.4 per cent) sales respectively. The premium side of each segment was won by BMW, with the X5 (3111 and -2.0 per cent) and X7 (840 and +6.2 per cent) taking a convincing lead.

Where smaller vans are concerned, it was Renault’s Kangoo that shot to the top with 508 unit sales (-30.6 per cent) while the larger portion of the segment was again ruled by the Toyota HiAce, with 8748 unit sales (-10.1 per cent).

Although van categories did decline slightly, the utility side of the light commercial market showed strong growth – especially for Toyota. In the two-wheel drive division, sales of the HiLux jumped 29.1 per cent to 17,062 units and on the four-wheel drive side of things the HiLux again topped the charts with 47,329 unit sales, up 19.6 per cent.

Toyota has topped the Australian sales charts for a couple of decades now, Holden’s VT-series Commodore the last model to beat Toyota to the top of the Aussie sales charts back at the turn of the millennium.

Indeed, Toyota outguns second-placed Mazda by a considerable margin – 12.5 market share points to be exact – and grew its sales figures by an impressive 3.3 per cent overall to tally 231,050 unit sales, or approximately one-fifth of the overall market.

Behind Toyota, Mazda sold 95,728 units (-5.3 per cent on 2021) ahead of Kia (78,330 and +15.3 per cent), Mitsubishi (76,991 and +13.7 per cent) and Hyundai (73,345 and +0.6 per cent).

The top 10 is rounded out by Ford (66,628 and -6.7 per cent), MG (49,582 and +27.1 per cent), Subaru (36,036 and -2.6 per cent), Isuzu (35,323 and -1.2 per cent) and Volkswagen 30,946 and -24.1 per cent).  Read more10th of January 2023  Incoming: Purple patch for new cars in 2023Vehicle production is bouncing back, meaning more choices for Aussie buyers in 20239th of January 2023  Market Insight: Toyota’s winning streakHybrids reach 31.5pc of Toyota’s sales in Aus amid cost of living, supply challenges |

Click to shareMarket Insight articlesResearch Market Insight Motor industry news GoAutoNews is Australia’s number one automotive industry journal covering the latest news, future and new model releases, market trends, industry personnel movements, and international events. Car Finance |

Connect with us

Facebook Twitter Instagram